Twitter and the Pursuit of Revenues

What happens when you cannot find new customers to sell your product to? Usually, you will try to squeeze out as much money as you possibly can from your current customers. That is precisely what is going on at Twitter HQ.

During 4Q14, Twitter added 4M users. During the year 2014, Twitter added 47M users, which brings the total monthly active users (MAUs) Twitter has to 288M. If you’re a heavy Twitter user, you probably love the service and can’t imagine living without it. If you merely like Twitter, you probably use it occasionally whenever you have some downtime. This brings us to the average Twitter user: they made an account to try Twitter, but never came back; either because they didn’t like the service, found no use for it, or as I’ve written many times before, found Twitter confusing.

So now we know that Twitter has a user growth problem, and for reasons above, the company can’t seem to get users to stay and use Twitter. We will circle back to MAUs later, but first let us check in with Twitter’s financials. You would think a company that isn’t gaining traction with the users is also not making much money, but you would be wrong. Before I begin discussing revenues, let me preface this by saying that Twitter is an extremely young company (it went public in November 2013), which means that there isn’t a large collection of historical data we an analyze. While that makes the job of the analyst harder since he is working with so many unknowns, it is invariably more interesting!

Revenues increased 33% QoQ, and 111% FY14 vs FY13. Whatever Twitter is doing to get more advertising dollars, it is working splendidly. The company now earns roughly half a billion dollars every quarter. It is still a tiny business, but the way Twitter has been able to grow revenues is impressive. Twitter expects to earn $440-$450M in 1Q15, which is a slight decline from this past quarters’ performance ($479M).

The first few years of a company after an initial public offering are always a mess, especially in terms of expenses. Usually, formal processes for expenses are not set up yet (employee credit cards, traveling costs, etc) and budgets are either nonexistent or valueless, since everything is constantly in flux. The company is tackling bigger issues such as growth and product, which makes the expenses side of things of secondary or tertiary importance. For these reasons, it is not fruitful to dive deep into the expenses of a young company such as Twitter - they’re not indicative of future trends.

There are some interesting things going on in Twitter’s expenses, though. R&D, as a percentage of revenues, has been diminishing for the last year. I believe this is happening because management feels the opportunity cost of investing in R&D is too high. Instead, that money is being spent on Sales and Marketing (S&M). Twitter spent $0.43 on each $1 it made on S&M in 2014, which would be an atrocious statistic if not for the immaturity of the company.

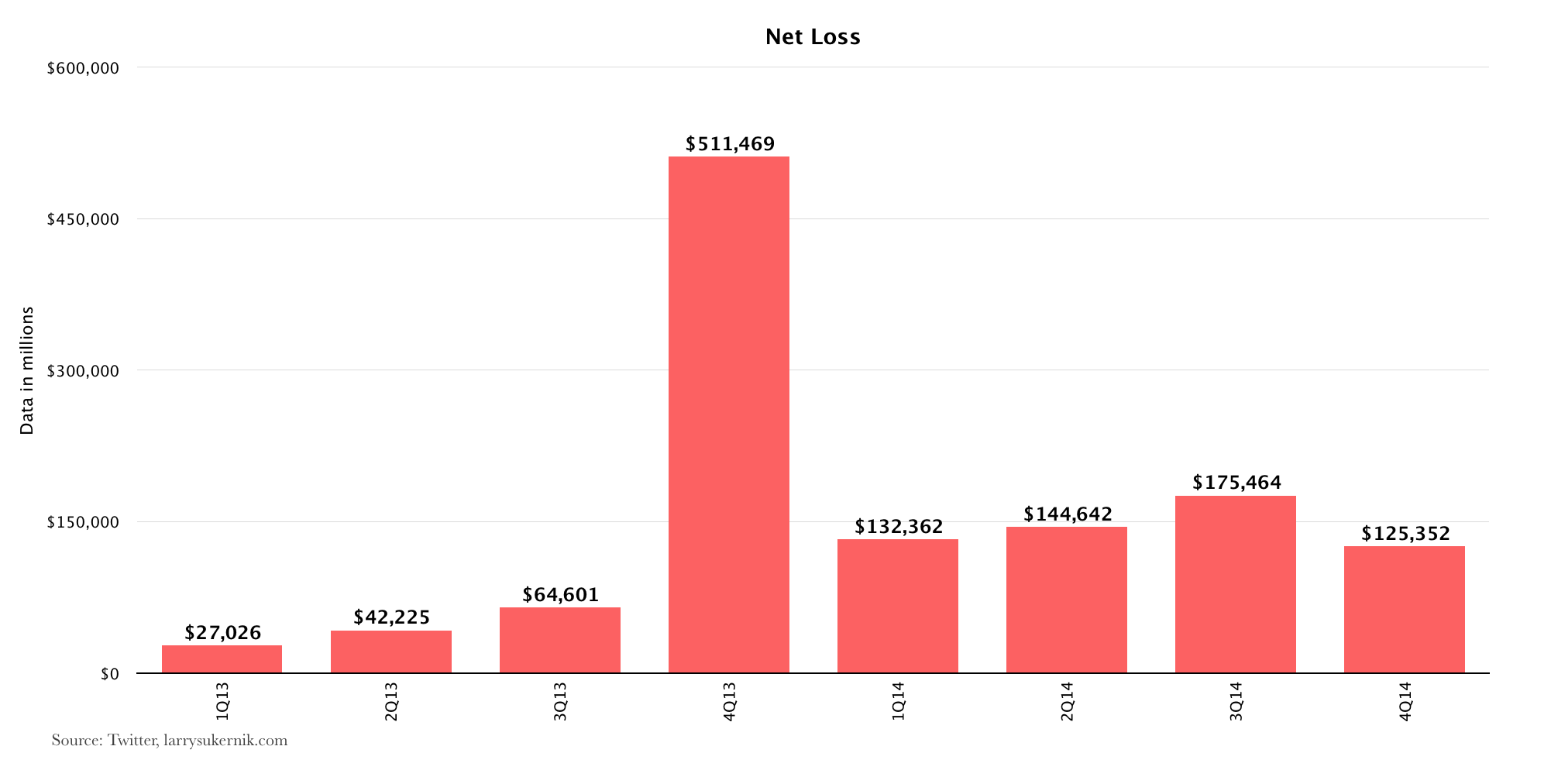

Twitter has never been profitable, and will likely continue posting net losses in the immediate future (1–2 years). You can look at Twitter’s net losses in one of two ways. As an investor, you should be risk-averse and be highly skeptical of Twitter’s ability to post a profit. Social networks come and go, internet bubbles burst and pop, but you aren’t going anywhere. Would Warren Buffet hold Twitter stock? Probably not. The alternative viewpoint you can take on Twitter is that you truly believe in the product and see it as an unbridled social network that advocates the freedom of information, or some other noble or cool pursuit. You may believe that Twitter represents freedom, and the profits will certainly come later, leading you to invest in the company despite continuous net losses. Which viewpoint you choose is a personal question, but now you are armed with the facts.

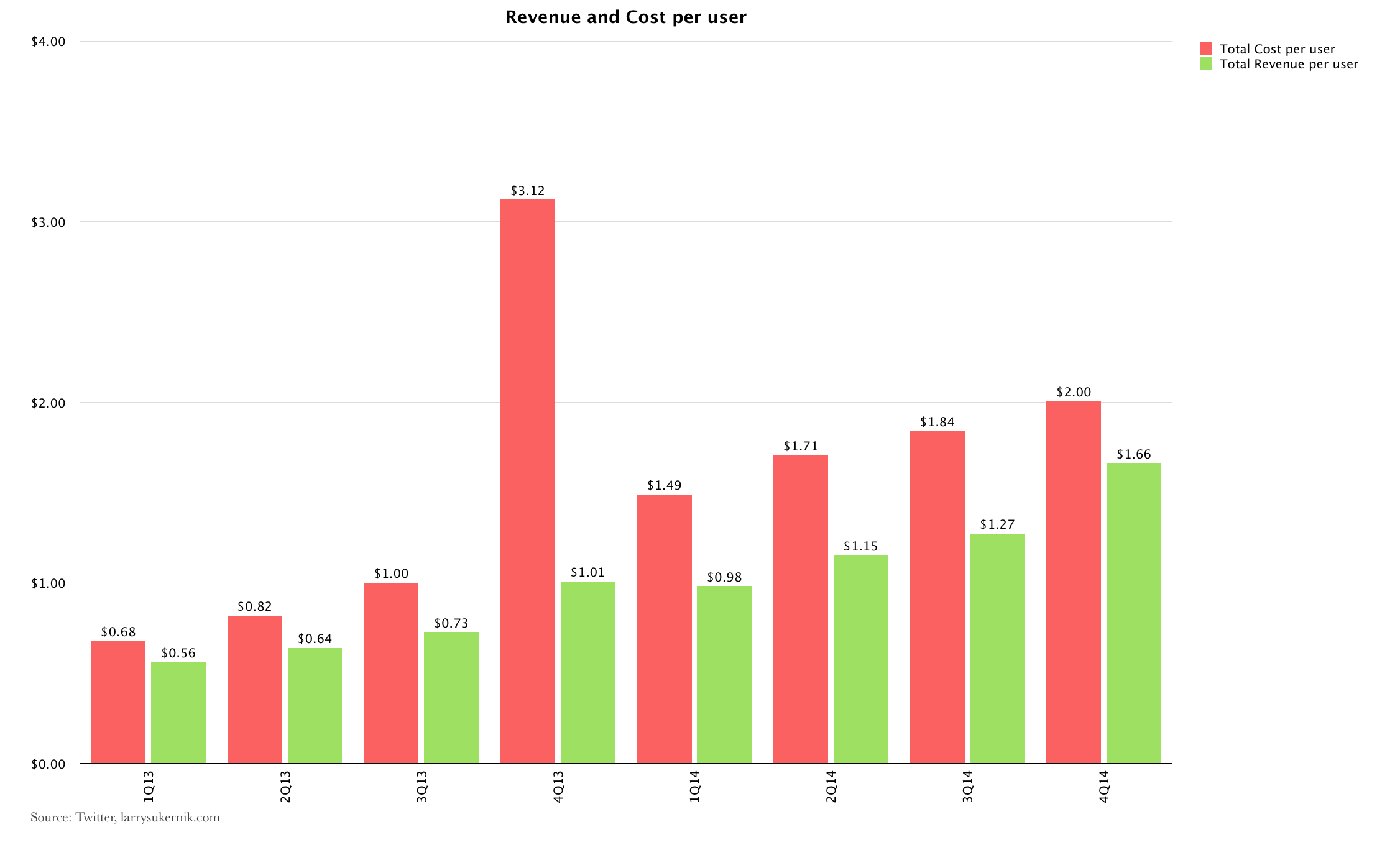

If we take all of Twitter’s revenues and expenses, and spread them over MAU, we will get two rough estimates of profitability: total revenue per user, and total cost per user. Although MAU may not be the best metric to use as the denominator, it is a more accurate representation of per-user profitability than “timeline views”, which is the other metric Twitter provides.

Unlike other analysts, I included all sources of revenue (advertising & licensing) as well as all expenses (cost of revenues, research and development, sales and marketing, and general and administrative) to compute per-user costs, because they provide the most comprehensive picture of profitability.

With that said, you can see for yourself that the total cost per user of running Twitter is higher than the total revenues - by approximately $0.34 per user in 4Q14. That is - Twitter is losing roughly 34 cents for every user of the service.

In Short

Given that Twitter is still such a young company, it is difficult to evaluate its performance in financial terms, since the expectations aren’t set yet. Twitter’s user growth, however, is a different story. MAU are not growing as fast as investors, and more importantly Twitter, would like to see them grow. Twitter probably has one more year to figure things out before investors start to really get antsy. As I’ve made abundantly clear before, the first problem I would tackle would be Twitter’s onboarding process, which remains a confusing mess. Twitter remains my favorite social network, and I remain rooting for the little blue bird even if it’s learning to fly very, very slowly.