Disrupting the Innovator's Dilemma

It seems Clayton Christensen has become the Michael Porter of the third millennium, having his book, The Innovator’s Dilemma (TiD), quoted in all sorts of articles, talks, and even other business publications. You can’t read a single WSJ or NYT article without seeing the word disrupted. Companies go out of business because they are disrupted by more innovative businesses. Products and services kill other products and services because they are so disruptive to them. A company even disrupts itself when it releases a new product that improves on the old one. Everybody is being disrupted everywhere, all the time.

Some Background

If you aren’t familiar with Christensen’s law, it is this. There are two types of technologies defined in his framework: sustaining technologies and disruptive technologies. In order to be as accurate as possible, I will quote his own definitions for these technologies.

“Most new technologies most improved product performance. I call these sustaining technologies…What all sustaining technologies have in common is that they improve the performance of established products, along the dimensions of performance that mainstream customers in major markets have historically valued.”

From the next paragraph…

“Occasionally, however, disruptive technologies emerge; innovations that result in worse product performance, at least in the near-term…Disruptive technologies bring to a market a very different value proposition than had been available previously. Generally, disruptive technologies underperform established products in mainstream markets…Products based on disruptive technologies are typically cheaper, simpler, smaller, and frequently, more convenient to use.”

So now you have a basic understanding of Christensen’s ideas. I still encourage you to read The Innovator’s Dilemma, since it shares many interesting ideas, but for our purposes, you are ready.

Opportunity Cost

One of Christensen’s fundamental contributions is quite profound. To summarize, it goes something like this. Management of a company doesn’t think about the disruptive, low margin technologies nearly as much as they do about higher margin technologies, since by definition, low margin products are not as profitable.

As Christensen himself admits, a company becomes successful in the first place from the processes, values, and ultimately products it created in the past. Since the goal of most companies is to be profitable, they must create profitable products. Profitable products are usually more expensive, provide more features (value) to the buyer, and/or carry with them an element of prestige. According to TiD, these very same products are ripe for disruption. Thus, companies should avoid being disrupted by instead investing in disrupting themselves, before somebody else can disrupt them.

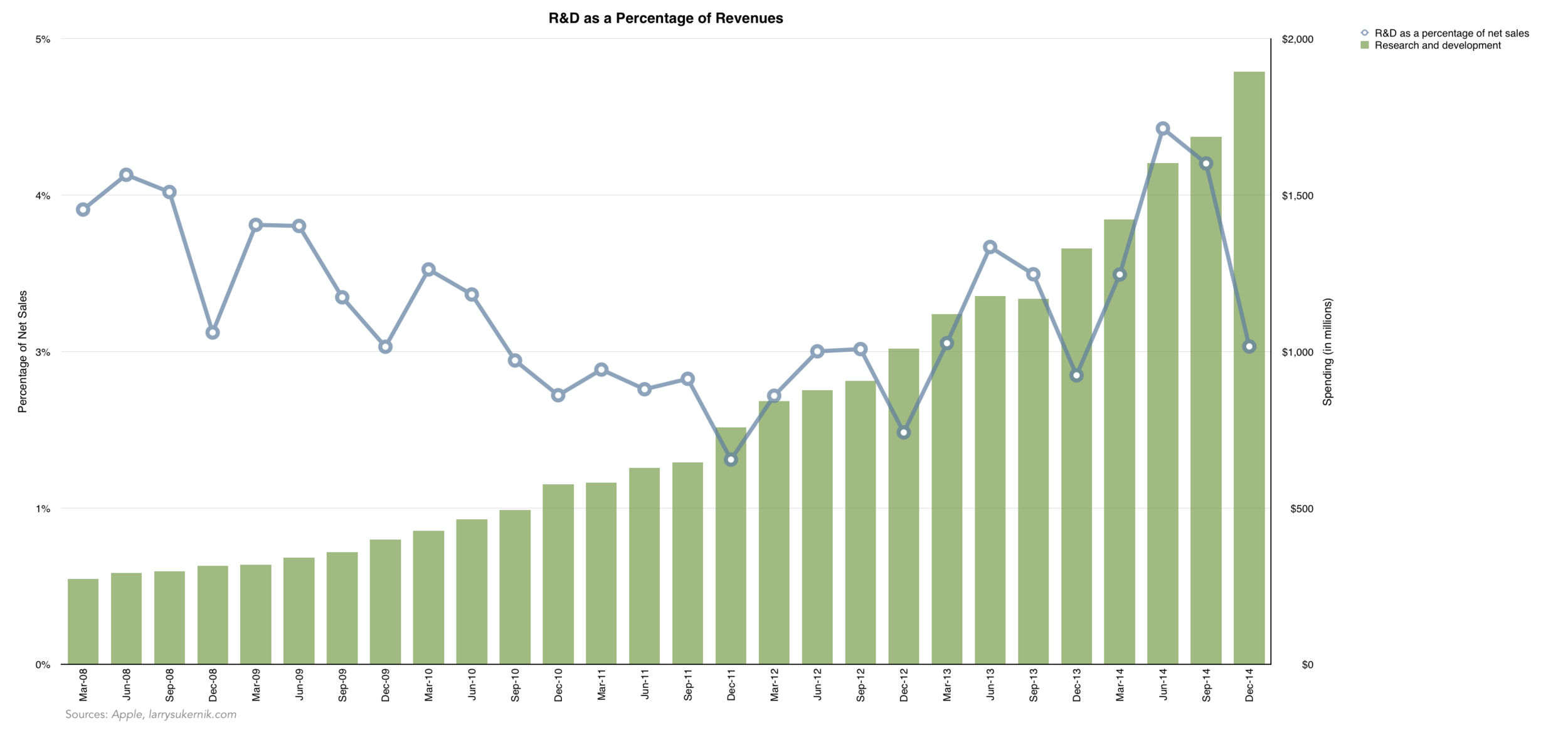

This all sounds great until the realities of the real world come in. Say you are a car company, and have $1B to invest. You can either invest in your current best-selling model in order to improve it, or you can invest in R&D for a cheaper, more economical car that you think would do well in developing nations. Absent other information, TiD would urge you to invest in the cheaper, low margin car, since it may become a disruptive technology in the future. So you go ahead and invest the $1B in this low margin car, and it becomes an international hit! Drivers in India, China, and Brazil are buying them in droves, and your production lines are busy churning out more and more vehicles. You smile at your production volumes, but then you look at your income. Turns out, the margins on these little guys are so low that you’re actually barely making any money on all of those sales! You tell yourself, don’t worry big guy, since you still have your high margin car available for sale, and you’ll make the profits that way. You open your trusty spreadsheet to check the latest sales figures, and lo and behold - the sales dropped! Immediately, you call the director in charge of the high margin car and ask him what went wrong. “We didn’t invest much in improving this model since we spent everything on the low margin car. Meanwhile, our competitors vastly improved the engines, their navigation system, and MPG of their cars, which stole away from our sales”. But you read The Innovator’s Dilemma, you say to yourself. How could everything have gone so wrong?

Now imagine that instead, you invested the high margin vehicle, which was already beloved by your customers. With the extra $1B in R&D, you were able to improve on the features you already offered, thus overpowering the new features your competitors offered.

For a business book, it is astounding that TiD fails to mention the opportunity cost of investing in a potentially disruptive technology. The costs of investing in disruption do not guarantee results. For large corporations with piles of cash, the opportunity costs of investing extra sums in finding a disruptive technology may be worth it. But large companies with limited cash may find themselves in an odd predicament, and disruption may be the last thing they need.

Sample Size

Christensen gives us examples disruptive technologies in action through the following industries: disk drives, excavators, and steel.

Acquiring large amounts of sample sizes for a business book of this nature is unfeasible for one person, especially in 1997, when TiD was published. You would have to get access to data from thousands of companies, explore each industry they are in, and find the products and companies being disrupted or disruptive. Instead, TiD gives us examples from a sample size of three, “proving” that disruptive technologies come in two varieties and are indeed what make or break companies. I’m sure you can see the ludicrousness in the preceding sentence yourself. A sample size of three is not enough to base a whole book on. TiD also implies that every industry gets disrupted in the same way, since it doesn’t say otherwise. Does the luxury clothing industry get disrupted by cheap knockoffs? What about expensive Swiss watches that are undercut by low cost Chinese fakes?

As an example, evidence of disruption is found only in five industries (1, 2, 10, 22, and 25), three of which were sampled by The Innovator's Dilemma. No evidence of disruption is found in the other industries.

Known-Unknowns and Known-Knowns

TiD is backed by a lot primary evidence. Christensen was able to speak to managers and CEOs to ask them what went wrong, and more importantly, what they did to fix it. Often times, the fix came in the form of a new, but internal venture, backed by the full faith and credit of the company CEO. This, in turn, allowed the company to create disruptive products, since the internal ventures were unshackled from the unyielding forces of resource allocation.

I will turn to former U.S. Secretary of Defense, Donald Rumsfeld for my next comment.

“There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we don’t know. But there are also unknown unknowns. There are things we don’t know we don’t know.”

We attribute our performance to our behavior - that is, we take credit for what we can measure and see. If a new CEO joins a company, and the sales figures go up, we ascribe the results to the new CEO. That is, after all, the only thing that changed from before to now. Unfortunately, this isn’t entirely true, and we attribute the increase in sales to the CEO because that is the only known we can identify. Many changes may have taken place, but none of these changes are visible or measurable by us. Continuing with our car analogy, perhaps the demand for low cost vehicles increased, which itself is the result of shifted consumer tastes. Consumer tastes were themselves influenced by something else. Perhaps the negative impact large vehicles have had on the environment led consumers to feel bad about their oversized vehicles, opting them over time to prefer smaller and cheaper alternatives. Is it possible to link the increase in sales to the change in consumer taste for smaller vehicles? Sure is possible, but it is much harder and considerably less obvious. Instead, you might attribute the increase in sales to the new CEO, who is a very obvious change.

Similarly, TiD substitutes unknowns with knowns in order to explain many of the strategies used by companies and their CEOs. A CEO may say the increase in sales would not have been possible if not for the newly funded internal venture, but how can he be so sure? Many of Christensen’s interviews were conducted before the advent of powerful computers that process terabytes of data, which makes the results even more dubious. Could it be that disruption is simply a known-unknown, rather than a known-known as TiD establishes it to be?

We know about the known-knowns. We know about the known-unknowns, but we cannot explain them. We don't know about unknown-unknowns, and therefore cannot explain them. TiD confuses the purple triangles with the green circles.

User Experience, Prestige, and Other Intangibles

You will have to use your prior knowledge of sustaining and disruptive technologies for this next passage, so if the definitions escape you, read them once more at the start of this post. If you remember them, let us continue. iPhone - is it a sustaining or disruptive technology? For starters, it came bundled with a web browser, a phone, and camera, none of which were wholly new technologies. The PocketPC, which came known to be as Windows Mobile, also offered all of those features. Thus, the value proposition of the PocketPC was the same, on paper, as that of the iPhone. The PocketPC flopped, while the iPhone prospered. Would that mean we could call the PocketPC a sustaining technology, and the iPhone a disruptive one? What makes the iPhone any more disruptive than the PocketPC? Playing devils advocate with myself, I would say the user experience of the iPhone was monumentally better, making it much more convenient to use. But as far as the value proposition - it was almost the same as that of the PocketPC.

When I was a young, puerile kid, my grandfather gave me a Casio calculator watch. I though it was the epitome of cool, and I wore it everywhere. My grandfather gave it to me because it looked futuristic, but also because he knew I would never wear a mechanical at that young age. My Casio checked off all the typical characteristics of a disruptive technology: it was in most cases cheaper than a mechanical watch, it was simpler to read time with, it weighed less, and it even provided me with the unprecedented value of having a portable calculator with me everywhere I went! Many years later, however, the mechanical watch industry is alive and well.

The above are only two examples that illustrate the shortcomings of TiD. The first example with the PocketPC and the iPhone attempts to show that despite the fact that both products are on paper disruptive technologies, that alone did not make them successful products. Much more is needed than just a new value proposition or a cheaper price. As Apple has shown through the years, a great user experience goes a long way. My Casio calculator watch also fit the bill to be labeled a disruptive technology, even though in retrospect we know there was nothing disruptive about it. Watches are often luxury goods that carry an element of prestige and social class with them. It may very well be that smartwatches will in the future provide so much value as to overpower that element of prestige, but the point remains - disruptive products may be disruptive in ways TiD did not foresee.

Performance Oversupply

Performance Oversupply (PO) is exactly what it sounds like: it is when a product gets packed with so many features and performance enhancements that it becomes more powerful than is required by the consumer. Thus, the consumer experiences diminishing returns from the performance of the product, since he can’t make use of it. A great example of PO are the latest computers that are being released. The average consumer doesn’t need all of the power that is packed into the machine, since all they will be doing is watching YouTube videos, browsing the web, and using some sort of word processor. In effect, the computer is more powerful than the power an average consumer needs from the computer. If we made a hypothetical power scale, the computer would be an 8, while the needs of the consumer would be a 5. The difference (8 - 5 = 3) is the Performance Oversupply.

Performance supply is an 8. Performance demand is a 5. Performance Oversupply = 8 - 5 = 3.

TiD contends that when a PO occurs, the technology is ripe for disruption. Going by the preceding case, you could argue the iPad/Chromebooks/Ultrabooks are the form of disruption Christensen was talking about, since they’re less powerful, cheaper versions of the PCs they replaced. These less powerful, “disruptive” technologies provide exactly, if not slightly less power, than the consumer desires. On our hypothetical power scale, they would score around a 4.8.

This all makes perfect sense - but there is another side to every coin. What if the needs of the consumer increase to match the PO? I find it best to explain through example, so let’s turn to one. YouTube is becoming television for the masses. More and more people are watching YouTube (or some other type of online video) every year, and as a result of technological improvements, the quality of these videos improve tremendously. YouTube now supports 4K UltraHD video, which requires much more processing power to consume. Not only is the world watching more videos, but a greater number of people are now editing and uploading their own videos. These content consumers and content creators are bridging the gap between the power demands of the consumer and the PO. Instead of a ranking of 5 for consumer needs, these consumers now rank a 7. Thus, the PO is reduced to (8 - 7 = 1). This suggests there might be room for Performance Oversupply, and disruption in this market may not happen after all.

Performance supply is an 8. Performance demand is a 7. Performance Oversupply = 8 - 7 = 1. The point of this illustration is to show that performance demand can increase, which in turn decreases Performance Oversupply.

For this example, the performance of the PC is kept stable at 8, since the rate of progress on processor technology has been slowing considerably in recent years, while consumer demands have been growing.

The Randomness Factor

This next commentary is similar to the Known-Unknowns and Known-Knowns point we touched on earlier, but it ventures a bit further, into new territory. The question I ask is as follows: does the whole of a disruptive technology come from what a company does in terms of productive effort (R&D, employees, management, etc…), or can a certain percentage of the technology be attributed to luck or randomness? In fact, TiD does make one brief reference to the element of luck in the success of a company, but it then proceeds to dismiss it almost entirely. Here’s what Christensen writes on the subject of luck:

“One might be to conclude that firms such as Digital, IBM, Apple, Sears, Xerox, and Bucyrus Erie must never had even well managed. Maybe they were successful because of good luck and fortuitous timing, rather than good management. Maybe they finally fell on hard times because their good fortune ran out. Maybe. An alternative explanation, however, is that these failed firms were as well-run as one could expect a firm managed by mortals to be - but that there is something about the way decisions get made in successful organizations that sows the seeds of eventual failure….The research reported in this book supports this latter view.”

Christensen is essentially saying that luck is not as important a factor as the processes for decision making. And he’s right in the grand sense - a company cannot attribute its success only to the element of luck, because it would have to consistently produce “lucky” products, which by definition, does not happen often. But in regards to disruptive technologies, which is precisely what the book is centered upon, luck is a crucial element. To better illustrate this point, let’s use a quote from Ed Catmull’s (the President of Pixar) book, Creativity, Inc.:

“When companies are successful, it is natural to assume that this is a result of leaders making shrewd decisions. Those leaders go forward believing that they have figured out the key to building a thriving company. In fact, randomness and luck played a key role in that success.”

So who are we to believe; the intelligent Harvard professor with years of experience, or the creative genius who helped spawn many of the worlds greatest animated films? I, for one, believe both are right…partially. Most people read TiD and treat it as the bible. I recommend reading it with a grain of salt. The processes of a company do indeed make-it-or-break-it, but luck is undeniably a critical factor too. The iPhone was a great product, but it also had fortuitous timing (luck), which is what made it so disruptive.

Luck and randomness is what happens in the dashed circle. Everything else in the larger circle is attributed to the productive efforts of the company. The size of the luck and randomness circle is arbitrary and used only to illustrate the idea.

No Book is Perfect

The Innovator’s Dilemma would have been a fantastic blog post, but as a book, it is extremely light on ideas and data points. As I have attempted to show through the above examples, there are a lot of points that TiD fails to explain. Basic economic concepts such as opportunity cost are left untouched by Christensen. Moreover, the sample size for the book is highly questionable. It often substitutes unknowns with knowns, and randomness with good decisions by managers. Intangibles are also oddly missing from TiD. Finally, while Christensen clearly shows how Performance Oversupply is a sign for an upcoming disruption, he keeps the power needs of consumers a static variable, which is demonstrably not a realistic assumption.

A disruptive product has become a business buzzword for good product which steals sales from the status-quo product. It is a word that explains the effect a product has had on the market, but not how that effect took place. It is an umbrella term for everything and nothing, all at once. While The Innovator’s Dilemma raises many excellent ideas, no book is without its faults and deserves to be read without skepticism. I will end this essay with a quote from Samuel Lee, an Assistant Professor of Finance at NYU.

There are two ways to validate an economic or financial theory: wait 100 years and collect new data, or look at a fresh new data set, such as another time period or different markets. It can take decades before someone’s held accountable for a bunk theory.

Since 100 years have not passed, I took the second approach.