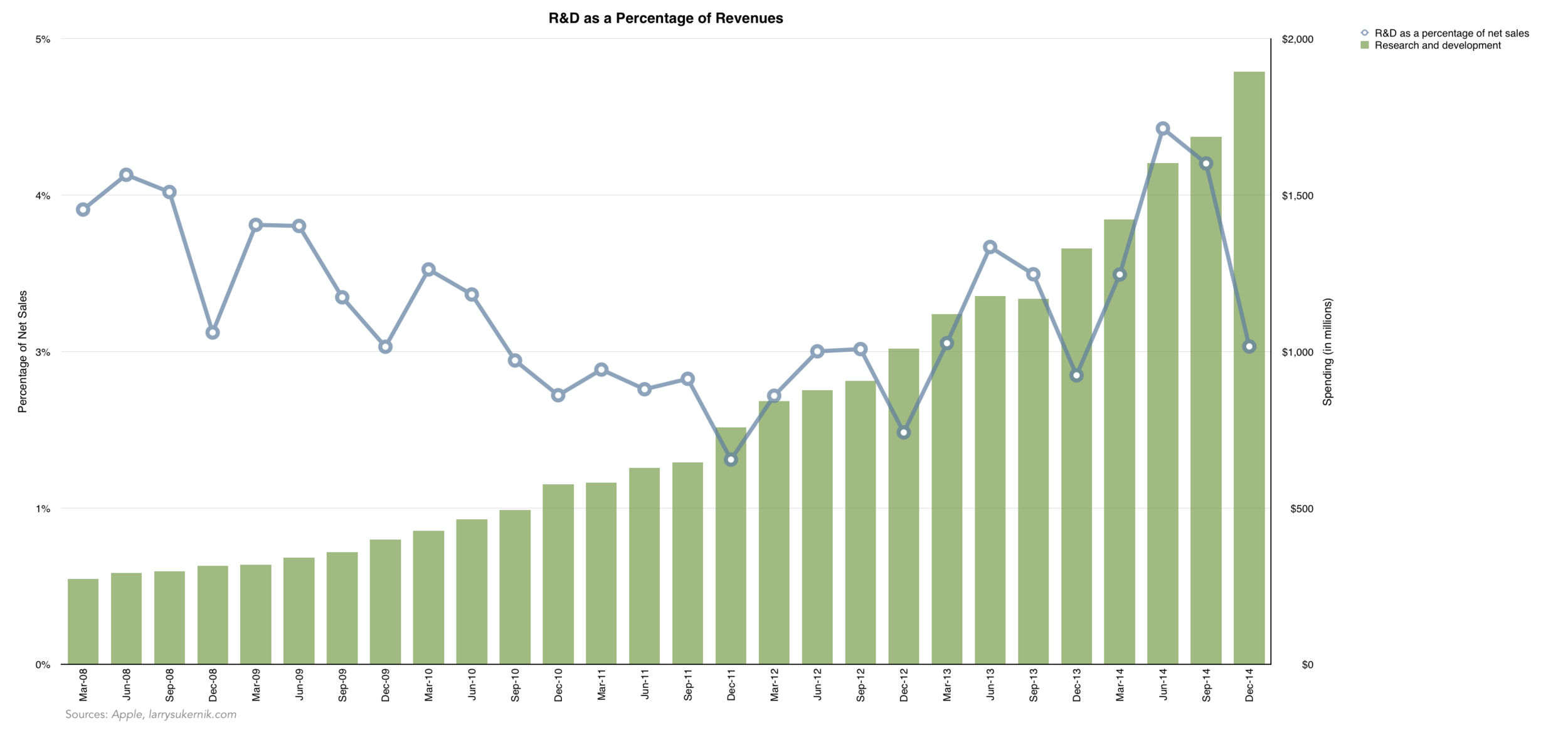

Accounting and Finance for the Future

In the last fifty years, the worlds of accounting and finance changed dramatically, mostly due to two factors: regulation and technology. I’ll leave the regulation part of out of this discussion for a later time, but the technology aspect is fair game for us.

In the old pre-computer days, the accounting and finance professions had to do everything by hand. To calculate the revenue of a company, you couldn’t just use a SUM function, you had to manually sum up all of the individual numbers with a calculator and a pen in hand. As you could imagine, mistakes were made often, and very difficult to find.

Enter computers and information systems. Digital spreadsheets such as VisiCalc, Excel, and QuickBooks came into existence, making the lives of number-crunchers phenomenally easier. One benefit of spreadsheet software was that you didn’t have to manually write everything out. Spreadsheets were efficient, in every academic sense of the word. Another was the timeless nature of digital records - they don’t expire with time (caveat: formats go out of style, and hard-drives fail, but compared to paper records spreadsheet software was a huge win for the profession). To be sure, ample negatives existed as well. It is potentially easier to get away with fraud since digital records can be easily deleted (especially if the fraudster is a member of management).

But this post isn’t a history lesson. In fact, it is quite the opposite. I included the discussion above just to give you a little glimpse into how the accounting and finance professions changed in the past few decades. I think it is a fair assumption than to say that they will continue evolving in the next few decades as well.

Accounting and Finance in the Future

You do not need to be a erudite to see that both accounting and finance will be moving into the cloud. In fact, much of it already has. Most large companies keep backups (and original copies) of their financial data in the cloud, purchasing proprietary or off the shelf solutions (in the consumer space we call it a product, but in enterprise it is a solution) from companies such as Microsoft, Salesforce, Box, and countless others. The future of all data is in the cloud. That pontification was easy.

But what about live, continuously updating financial information? Traditionally, management, investors, and other company stakeholders would request monthly, quarterly, and annual financial disclosures. These disclosures are heavily regulated by the PCAOB, SEC, AICPA, and countless other governmental and administrative agencies. The data often takes a lot of time to compile, since it’s housed in various locations, segregated to many employees, and needs to be audited before release.

But what if this would be a nearly instantaneous and live process in the future? As often is the case with this blog, let me explain through example. You’re a manager and you want to know how many sales your business line made this week, how much you already received in cash, and how much is still due from customers who have not paid up yet. In most companies, this fairly simplistic analysis would begin with the manager (you) emailing an associate for the data, followed by the work being performed by the associate. This work could take anywhere from 10 minutes to a few days to complete, depending on the company. If it is a more tech savvy company, you might have access to “Business Intelligence” graphs and charts which allow for some quick, glance-able and manipulable data. But even at the tech savvy companies, instantaneous data isn’t common.

Now imagine how accounting and financial information should be. As soon as a sale goes through, you can see the “Revenues” increase instantly, as well as a corresponding increase in “Cost of Goods Sold”. There is also a bar chart to show you sales trends over the past few days and months, that also gets continuously updated every time a sale is made. Continuing with our previous example, you can see that with every sale you make, your “Accounts Receivable” increases, as the customer owes you money on what they purchased and have not paid for yet. Every transaction that can be accounted for in the information system is accounting for in the system (this exists now). But every transaction is also categorized instantly, every account balance updated, every chart redrawn…everything is constantly up to date across the entire accounting system, which sits in the cloud. The data is simple to understand, quickly comprehensible, and immediately available for private and public consumption (imagine how happy investors would be). We got a man to the moon in 1969. We should be able to make one more giant leap, this time for accounting and finance, by 2020.